Strategy with Chipotle (CMG) and Texas Roadhouse (TXRH)

Discover a defensive Long/Short equity strategy focusing on the restaurant sector during volatile times. This analysis contrasts Chipotle Mexican Grill's scalable, high-growth business model against Texas Roadhouse's margin challenges and slower growth, offering a hedged relative value play within the industry.

Hi everyone,

Today we are focusing on Chipotle Mexican Grill (CMG) and Texas Roadhouse (TXRH).

We are sharing a Long/Short equity strategy in the restaurant industry. This strategy could be particularly appealing during periods of high volatility and uncertainty, as the ones we are facing right now, as this sector is generally considered more defensive and stable.

This pair trade is built on the premise that Chipotle Mexican Grill (CMG) is a structurally superior business with higher growth potential, strong operational efficiency, and scalable margins, while Texas Roadhouse (TXRH) is facing headwinds from rising costs, declining same-store sales growth, and operational inefficiencies.

CMG trades at 42x forward P/E and ~35x forward EBITDA/EV, which may seem expensive relative to peers, but the multiple reflects its high growth profile, superior margins, and significant runway for store expansion. However, any slowdown in growth or margin expansion could lead to multiple compression.

Chipotle Mexican Grill (CMG)

Business Overview

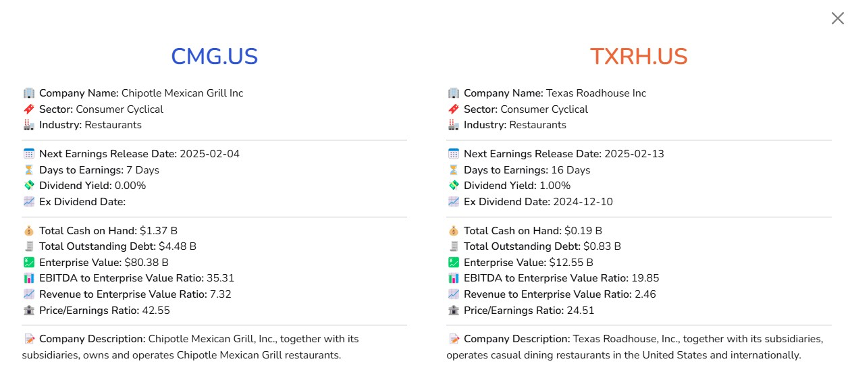

Chipotle Mexican Grill (NYSE: CMG) operates in the fast-casual dining segment, specializing in customizable, high-quality Mexican-inspired cuisine. The company has over 3,200 locations, with significant growth opportunities in North America and potential international expansion. CMG is differentiated by its focus on fresh, responsibly sourced ingredients and its innovative digital platform.

Growth and Margin Expansion Play

Consistent Revenue Growth Driven by Innovation and Digital Expansion

- Digital Transformation

- Menu Innovation: Recent launches, such as the viral fajita quesadilla and plant-based chorizo, demonstrate CMG’s ability to innovate.

- Store Expansion: CMG plans to open 250–300 new locations annually.

Scalable Operational Model

- Margin Expansion: CMG is targeting restaurant-level operating margins of 25%, driven by labor efficiencies.

- Economies of Scale

Texas Roadhouse (TXRH) Stock Analysis

Business Overview

Texas Roadhouse (NASDAQ: TXRH) operates in the casual dining segment, specializing in steaks and American fare. The company has over 700 locations, primarily in the United States, with a smaller footprint internationally. TXRH emphasizes in-restaurant dining, with a focus on family-friendly experiences and affordable meals.

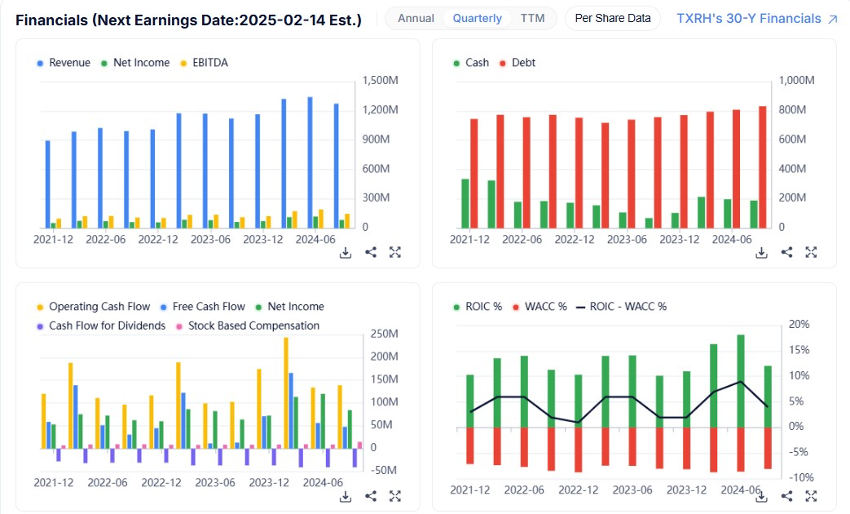

Margin Contraction and Slower Growth

- Declining Same-Store Sales Growth

- Rising Labor Costs: TXRH’s labor-intensive model is a significant headwind. Rising wages are disproportionately impacting the casual dining segment, where labor costs account for 34–36% of revenue. This contrasts sharply with CMG’s lower labor costs (~25%) due to operational efficiencies.

- Commodity Inflation: Protein prices, particularly beef, are a significant cost component for TXRH. The company lacks the pricing power that CMG enjoys.

Key Risks to the Thesis

Investment Risks

- Valuation Premium: CMG trades at 42x forward P/E and 35x EV/EBITDA, significantly above the restaurant industry average.

- Commodity Price Volatility: CMG is exposed to price fluctuations in avocados, chicken, and other key ingredients, which could pressure margins if cost increases cannot be passed on to customers.

- Execution Risks: CMG’s aggressive expansion plans carry risks.

Conclusion

This pair trade capitalizes on the structural divergence between CMG’s scalable, high-growth business model and TXRH’s margin-challenged, slower-growth profile. Long CMG and short TXRH is a compelling way to express a relative value view within the restaurant sector, while hedging against broader industry risks.

Unusuals

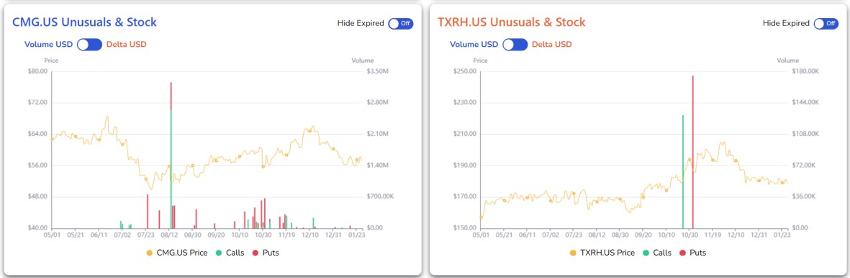

Regarding unusual options activity, CMG shows significant activity, particularly in August 2024, when an unusually large call worth approximately $2.80M occurred.

Following this, CMG's stock price steadily rose, peaking in October.

In contrast, TXRH exhibits relatively limited unusual options activity. However, the activity is more balanced, with call and put volumes being similar in size.

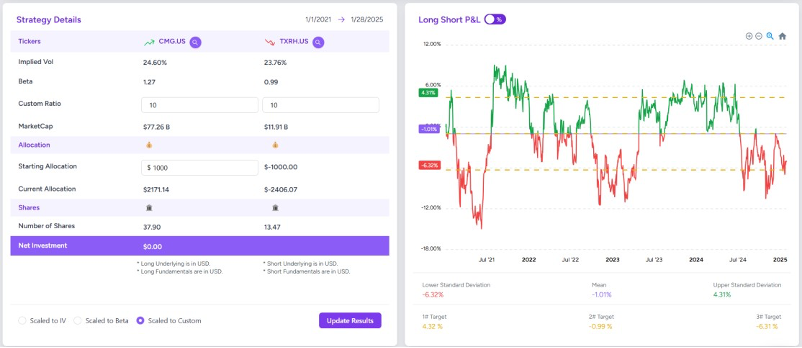

Long/Short Position

The deviation of this long/short is currently at -5.28%. As of writing this article, CMG is trading at $57.28, compared to TXRH $178.62 a share.

The suggested sizing will be scaled to a custom (10:10) ratio, due to similar IV and linear regression, with a long position of 37.90 shares of CMG at the current price of $57.83 ($2,171.14), and a short position of 13.47 shares of TXRH at the current price of $178.62 ($2,406.07).