Unlocking the Biotech Sector: A Strategic Long-Short Investment Opportunity

Explore a biotech long-short strategy: AbbVie’s strong cash flows and M&A vs. Vertex’s concentrated CF risk. Leverage market volatility and mean reversion for balanced gains and reduced portfolio risks.

Hello everyone,

Today we present a long-short in the biotech sector. This long-short strategy could be a valuable opportunity to capitalize on the growth of the biotech sector, driven by innovation and consolidation trends. The sector has shown resilience and growth potential, with increasing demand for novel therapies and advancements in areas like gene editing and immunology.

According to Bill Ackman, the potential policy environment under Trump’s presidency could lead to a significant uptick in mergers and acquisitions (M&A) within biotech. Factors such as corporate tax incentives, reduced regulatory hurdles, and pro-business policies may encourage large pharmaceutical companies to acquire smaller biotech firms with promising pipelines. Historically, such environments have fueled robust M&A activity, creating opportunities for investors to benefit from strategic consolidations. Watch it on X

AbbVie Inc. is a global biopharmaceutical company headquartered in North Chicago, Illinois. The company was established in 2013 as a spin-off from Abbott Laboratories, focusing on innovative medicines and therapies for serious illnesses.

Vertex Pharmaceuticals specializes in developing transformative medicines for serious diseases. Its dominance in the cystic fibrosis (CF) market is unparalleled, providing it with consistent revenue and funding for diversification. With products like Trikafta, the company addresses nearly 90% of CF patients worldwide. Headquartered in Boston, Massachusetts, Vertex has established itself as a leader in biotech innovation.

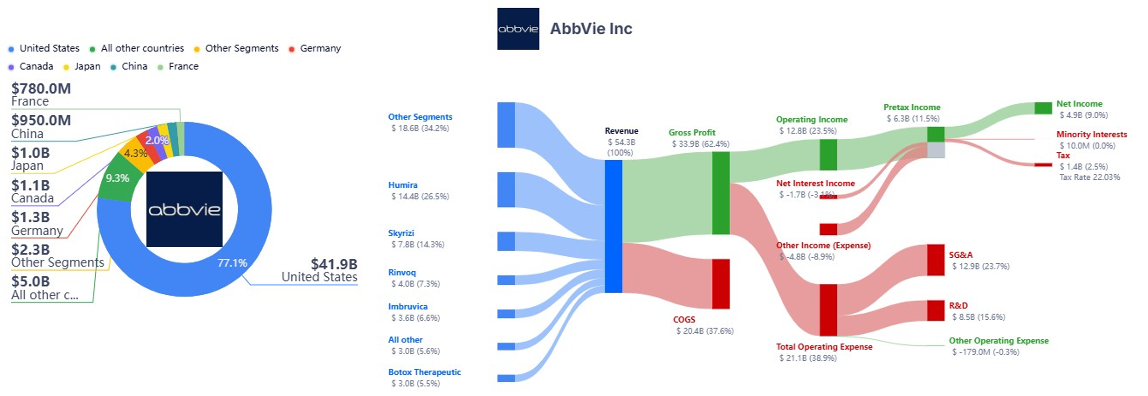

AbbVie operates primarily in two key segments. Immunology and Oncology and Neuroscience. Regarding Immunology, they have Products like Humira (adalimumab), a blockbuster drug for autoimmune diseases, which has been a significant revenue driver. Newer immunology drugs, such as Skyrizi and Rinvoq, are intended to offset Humira's declining revenues due to patent expirations. In oncology and neuroscience, it includes treatments like Imbruvica and Venclexta for blood cancers, and Vraylar for psychiatric disorders.

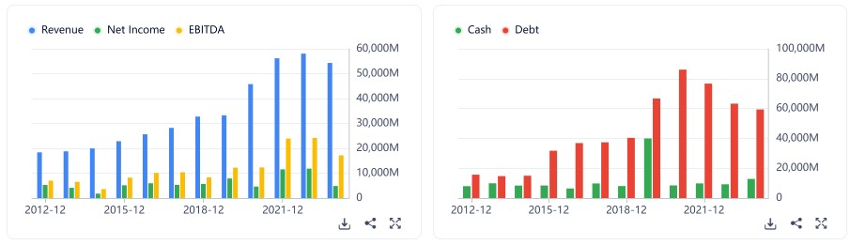

AbbVie has consistently delivered strong revenue growth, driven by its diverse product portfolio as we can see in the images below. Despite challenges like the loss of Humira's exclusivity in major markets, AbbVie has managed to maintain profitability due to cost efficiencies and strong performance of newer drugs. Nevertheless, AbbVie has a high debt load, primarily due to its $63 billion acquisition of Allergan in 2020. However, it has been aggressively paying down debt, as seen in the chart below. Dividend Yield is round 3.7%–4.0%, significantly above the S&P 500 average.

That said, a significant portion of AbbVie’s revenue (77% in 2023) is derived from the United States. While geographic concentration can pose risks in certain market conditions, it can also be advantageous in the current environment. The strong U.S. dollar enhances the company's purchasing power for imports and shields revenues from unfavorable foreign exchange effects, particularly during global economic uncertainty. This domestic focus helps mitigate currency risks that companies with higher international exposure might face.

ImmunoGen: AbbVie closed a $10.1 billion deal to acquire ImmunoGen, which strengthens its oncology pipeline, particularly with Elahere, a promising treatment for ovarian cancer. This acquisition aligns with AbbVie's strategy to offset revenue losses from declining Humira sales due to biosimilar competition. Source

Aliada Therapeutics: AbbVie announced plans to acquire Aliada for $1.4 billion to bolster its neuroscience portfolio. Aliada focuses on advanced blood-brain barrier technology, which could enhance treatments for Alzheimer's disease and other CNS conditions. Source

These acquisitions reflect AbbVie’s interest in securing innovative assets in high-growth areas like oncology, neuroscience, and immunology. They also underscore its potential to leverage M&A activity as a key growth driver.

In the near term, AbbVie appears poised to continue pursuing strategic acquisitions, given its history and current focus on diversifying its portfolio post-Humira. This trend could present opportunities for investors looking to gain exposure to biopharma consolidation.

Vertex Pharmaceuticals (VRTX)

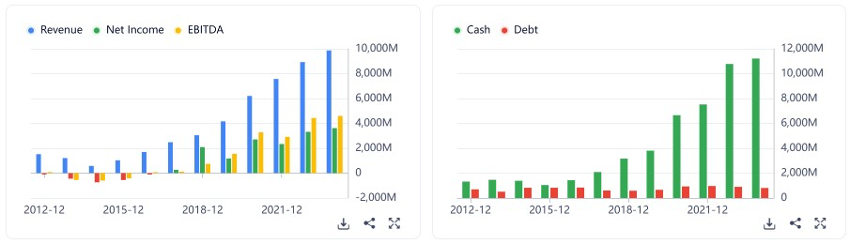

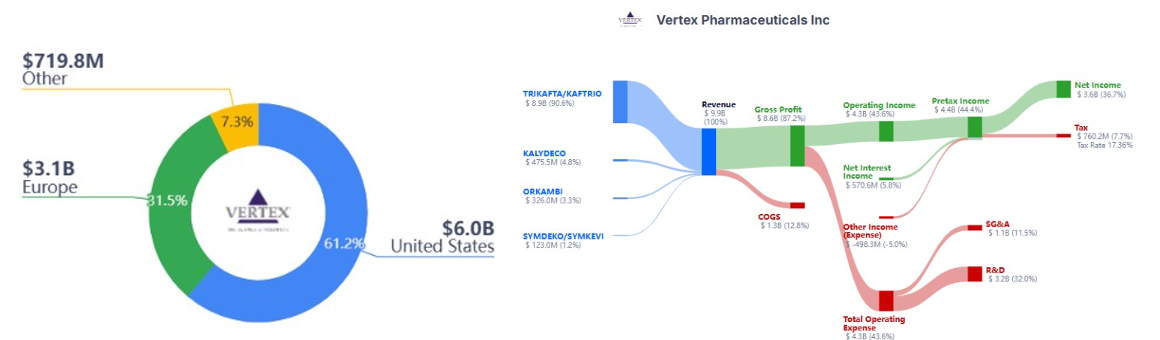

Vertex generated approximately $9.6 billion in 2023, with CF treatments contributing over 90% of this total. Revenues are projected to grow as the company expands into other therapeutic areas. It has maintained high margins due to limited competition in CF therapies and premium pricing. Net income exceeded $3.3 billion in 2023.

Regarding the remaining pipeline, there is Exa-Cel (CTX001), A gene-editing therapy for sickle cell disease (SCD) and beta-thalassemia. Then they have VX-548, that is a non-opioid painkiller targeting acute pain, currently in Phase III trials. This drug could disrupt the pain management market.

Regarding the risks in Vertex, there are a few. First, there is pipeline dependence. Despite diversification efforts, Vertex's financial health is still heavily reliant on CF drugs. As we can see in the image above, 90% of the revenue comes from KAFTRIO. There is some pipeline uncertainty too. While exa-cel and VX-548 show promise, they face regulatory hurdles and competitive risks.

Pricing Pressures: As Vertex continues its global expansion, particularly into cost-sensitive regions, the company may face downward pricing pressures. High-priced therapies like Kaftrio could encounter resistance in markets with stricter healthcare budget constraints or pricecontrol regulations. This challenge may limit the company’s ability to achieve robust revenue growth outside premium-priced markets like the U.S.

Currency risk: With 31.5% of Vertex’s revenue denominated in euros and the euro trading around 1.05 USD, currency fluctuations pose a significant risk. A weaker euro translates into reduced revenue when converted into U.S. dollars, negatively affecting the company’s reported earnings.

Considering that 30% of Vertex’s revenue is generated in Europe, currency risk represents a material financial exposure. Any adverse exchange rate movements may impact performance metrics.

The recent 17% decline in AbbVie stock price appears to have sparked unusual options activity, signaling potential investor optimism regarding a stock turnaround despite the setbacks in Phase II trials for its schizophrenia drug. Although the trial failures were a disappointment, the surge in options activity suggests that investors may be positioning themselves for a rebound. This could be driven by expectations of AbbVie’s ability to recover from this setback.

This development could present an interesting opportunity for a long-short strategy in AbbVie, as the biotech sector remains dynamic, with market sentiment often reacting swiftly to such clinical updates. Investors may look to capitalize on the potential for AbbVie’s stock to stabilize or rebound as new catalysts, such as upcoming trial data or corporate developments, unfold.

In the context of a long-short strategy, these dynamics in AbbVie could be combined with positions in other biotech stocks with differing risk profiles, leveraging the volatility while hedging against potential market overreactions.

The short position in VRTX can work well here. As we stated before, the recent currency risks and high expectations baked into its price, combined with concentration risk in CF and potential delays in its innovative therapies, make Vertex vulnerable to valuation correction.

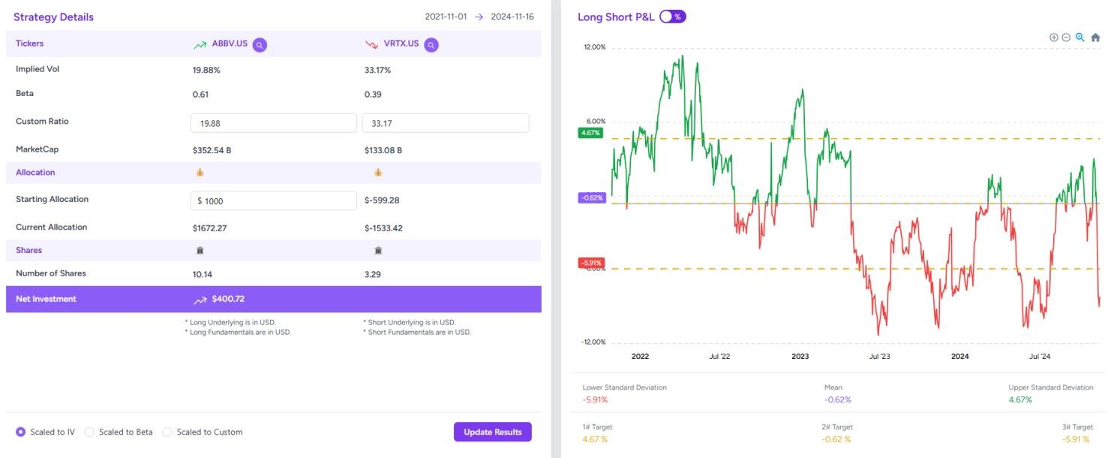

Long Short

This long-short strategy, which began on November 1, 2021, and goes until November 16, 2024, demonstrates a clear correlation between AbbVie (ABBV) and Vertex Pharmaceuticals (VRTX). Throughout this period, the stocks have consistently reverted to their mean, enabling the strategy to generate attractive returns. With an initial investment of $1,000, the current allocation consists of going long 10.14 shares of ABBV and shorting 3.29 shares of VRTX, resulting in a net debit of $138. The strategy is scaled based on implied volatility, as Vertex has a higher IV at 33.17% compared to AbbVie’s 19.88%, ensuring balanced risk exposure and preventing the higher volatility of Vertex from dominating the portfolio. This approach effectively captures periodic divergences and mean reversion while leveraging the strengths and weaknesses of both companies, showcasing the potential of long-short strategies to profit in the biotech sector.